The Role and Development of Decentralized Exchanges (DEXs)

Estimated Reading Time: 6 minutes

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 minutes to learn more

Decentralized exchanges (DEXs) are essential components of the digital asset ecosystem. They provide a gateway to the on-chain economy, enabling listing, trading, and liquidity provision across markets without the need for intermediaries.

Characteristics of Decentralized Exchanges and AMMs

In light of the recent Wells Notice issued by the Securities and Exchange Commission (SEC) to Uniswap Labs, it is important to highlight the unique attributes of DEXs. Although the SEC’s specific concerns have not been fully disclosed, their intent to potentially regulate DEXs echoes actions taken against major centralized exchanges like Coinbase and Binance, particularly regarding the classification of traded assets as securities. However, DEXs operate fundamentally differently from their centralized counterparts.

Most DEXs are powered by automated market makers (AMMs). Unlike traditional exchanges, which depend on centralized order books and market makers to match counterparties, AMMs use pricing algorithms to determine the price and liquidity of tokens in a pool. These pools are supplied by liquidity providers (LPs), who earn trading fees proportional to their contributions. This system fosters an environment where users retain control over their funds.

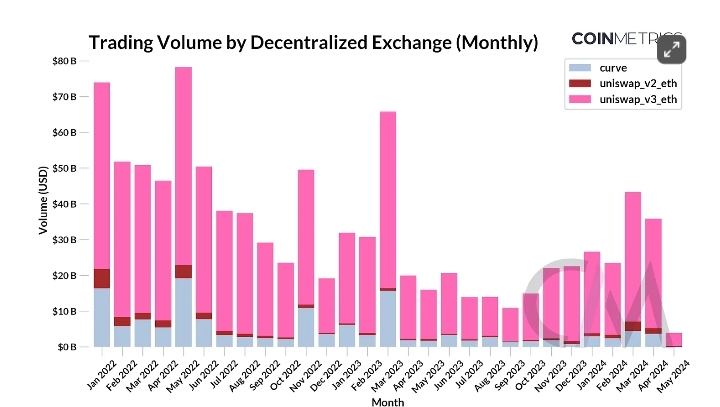

Trading Volume Rises

Rising Trading Volumes on Major Decentralized Exchanges (DEXs)

Trading volumes on major decentralized exchanges (DEXs) are experiencing an upward trend. Despite occasional spikes due to market volatility, trading volumes remained relatively low for much of last year, averaging around $15 billion in monthly volume.

However, since October, Uniswap has seen significant growth, recording a quarterly trading volume of $54 billion in Q4 2023 and $84 billion in Q1 2024. Curve Finance is also experiencing increased trading volumes, though they have not yet returned to the levels seen before the USDC de-peg in March 2023.

Uniswap: Leading Markets and Liquidity Pools

Uniswap currently holds the position as the largest decentralized exchange by volume, with over $2 trillion in cumulative transaction volume. It is a key player in the expansion of the decentralized finance (DeFi) sector. Each iteration of Uniswap’s protocol has brought improvements to its liquidity provision model.

Uniswap v2, introduced in 2020, offered a foundational AMM platform using a constant product invariant (x * y = k). This version enabled token swaps by ensuring liquidity even in less active markets. Its permissionless market creation process has supported a diverse range of trading pairs, from blue-chip tokens to memecoins.

Although Uniswap v2’s trading volumes do not match those of Uniswap v3, several pools on v2 feature a higher number of trades, benefiting newly-listed tokens and passive liquidity providers. However, this version also faced challenges such as susceptibility to maximal extractable value (MEV) exploits, reduced capital efficiency due to capital allocation across the entire price range, and the risk of impermanent loss, which can diminish earnings for liquidity providers.

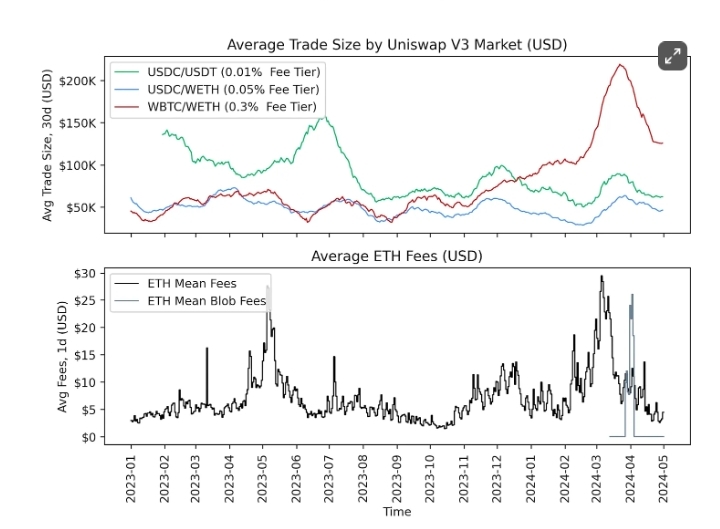

Impact of Protocol and Network Fees

Protocol-level trading fees (e.g., Uniswap v3) and network-level transaction fees (e.g., Ethereum mainnet or Layer-2 solutions) significantly influence trader and liquidity provider behaviors on DEXs.

The chart below illustrates that higher fee tiers, such as the 0.3% fee for the WBTC/WETH pair on Uniswap v3, tend to result in larger average trade sizes compared to lower fee tiers, like the 0.01% fee for the USDC/USDT pair. These fee tiers, along with external market conditions and transaction costs, directly affect the risk-return trade-off for traders and liquidity providers (LPs).

Trends Shaping the DEX Landscape

With the advent of various Ethereum rollups and layer-1 blockchains like Solana significantly reducing transaction fees, DEXs are now expanding across multiple networks. Uniswap v3, for instance, is deployed on 16 different chains. Several layer-2 solutions host native DEXs such as Aerodrome, the largest exchange on Coinbase’s Base network, facilitating cross-ecosystem navigation.

Others, like Raydium and Hyperliquid, offer hybrid AMM or order-book-based DEXs, leveraging high throughput and low fees. This variety caters to users with diverse risk profiles and preferences and will continue to evolve as rollups and layer-1 blockchains mature.

Uniswap is set to introduce its 4th iteration, featuring a “singleton” architecture where all pools reside within a single smart contract. This innovation will drastically reduce gas costs by eliminating the need for tokens to move between separate pool contracts during swaps. Uniswap v4 also introduces “hooks,” enabling developers to customize pool functionality and execution.

This enhances the protocol’s flexibility, allowing for the creation of on-chain limit orders, MEV protection tools, or custom logic for trading tokenized real-world assets (RWAs). Overall, the trends indicate that DEXs are becoming more universal, expanding across networks while catering to a broader spectrum of traders and liquidity providers.

Conclusion

The advancements in decentralized exchanges like Uniswap and Curve Finance underscore major progress in the DeFi sector, especially in optimizing liquidity management and trading efficiency. These innovations accommodate a wide range of trader preferences and risk profiles, suggesting a strong future for decentralized trading platforms.

As accessibility and efficiency remain key drivers, the crypto ecosystem is set to see broader adoption. Moreover, as the DeFi landscape evolves, regulatory frameworks and adoption trends around DEXs are expected to keep adapting.