Beyond Fiat: Can Stablecoins Become the New Credit Card Network?

Estimated Reading Time: 7 minutes

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. Take 2 minutes to learn more

The rise of stablecoins has the potential to revolutionize the financial landscape, and understanding their potential requires looking beyond the technology itself. By examining the successes and strategies of established credit card networks, we can gain valuable insights into the key factors driving adoption and the challenges that lie ahead for stablecoin ecosystems.

Stablecoins are transforming finance, much like credit cards once did, by enabling seamless global transactions with low fees and near-instant settlements. With over $150 billion in market capitalization and major players like USDT, USDC, and DAI, the stablecoin market is rapidly growing. Their reserves offer lucrative opportunities for custodians, and it’s likely that major financial institutions will develop their own stablecoins. Drawing lessons from the evolution of credit card networks can provide valuable insights into driving adoption, avoiding pitfalls, and ensuring long-term success in this dynamic space.

From Plastic to Pixels: How Credit Card Networks Can Inform Stablecoin Development

To the end-user, whether consumer or merchant, all stablecoins should ideally function as interchangeable representations of a dollar. However, the reality is far more nuanced. Each stablecoin issuer employs distinct mechanisms for issuance, redemption, and reserve management, leading to variations in stability, risk profiles, and regulatory compliance. Navigating this complex landscape will require sophisticated solutions.

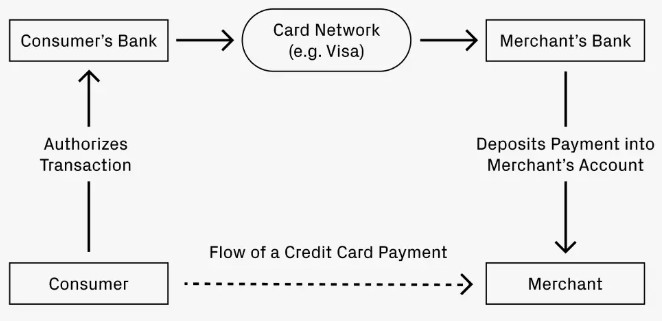

This scenario bears striking resemblance to the credit card ecosystem. Consumers utilize credit cards, essentially loans denominated in dollars, yet these loans are not entirely fungible due to varying creditworthiness. Credit card networks like Visa and Mastercard act as intermediaries, orchestrating the flow of funds between the card issuer (the consumer’s bank) and the acquirer (the merchant’s bank). This complex network involves multiple stakeholders with diverse interests, mirroring the potential dynamics within the evolving stablecoin ecosystem.

To illustrate this further, consider a simple credit card transaction. When you dine at a restaurant and pay with your card:

- Your bank (the issuer) authorizes the transaction and transmits funds to the restaurant’s bank (the acquirer).

- A network like Visa or Mastercard facilitates this fund transfer and collects a small fee for its services.

- The acquirer then credits the restaurant’s account with the transaction amount, minus a processing fee.

This example highlights the intricate network of players and processes involved in even the most basic credit card transaction, providing valuable insights into the potential complexities of interoperability and settlement within the evolving stablecoin ecosystem.

Stablecoin Networks: A Roadmap for Innovation Inspired by Credit Card Models

Imagine attempting to pay with stablecoins. Your bank, Bank A, issues AUSD, while the restaurant’s bank, Bank F, utilizes FUSD. Despite both representing the US dollar, these are distinct stablecoins. Since the restaurant’s bank only accepts FUSD, how does your AUSD payment get converted?

This scenario strikingly resembles credit card transactions:

- Your bank (the AUSD issuer) authorizes the payment.

- An orchestration service facilitates the conversion from AUSD to FUSD, typically charging a small fee. This conversion can occur through various mechanisms:

- Path 1: Direct stablecoin-to-stablecoin swaps on decentralized exchanges like Uniswap, often with minimal fees (e.g., 0.01%).

- Path 2: Redeeming AUSD for US dollars, then depositing those dollars with the acquirer to issue FUSD.

- Path 3: Netting flows across the network, where orchestration services offset opposing transactions, becoming more efficient at scale.

This framework reveals key parallels between credit card and stablecoin networks. It also highlights areas where stablecoins can significantly surpass traditional card systems:

- Cross-border Transactions: Credit card networks often impose exorbitant fees (e.g., 3%) for international transactions. In contrast, stablecoin conversions on decentralized exchanges can be executed for as little as 0.05%, a 60-fold reduction. This dramatic fee reduction has the potential to significantly boost global economic productivity.

- Business-to-Individual Payments: Stablecoins facilitate near-instantaneous settlements, enabling businesses to disburse funds rapidly. This is particularly valuable for businesses with global workforces, where frequent and substantial cross-border payments are common.

Identifying Opportunities:

Just as the credit card industry spawned major players in orchestration, issuance, and form factor innovation, the stablecoin ecosystem presents fertile ground for new ventures.

- Orchestration: Moving money is a lucrative business. Visa, Mastercard, and other major players in the credit card industry boast valuations in the tens of billions of dollars. The emergence of multiple competitive stablecoin orchestration networks is highly probable, mirroring the credit card market. While the stablecoin infrastructure is still evolving, significant opportunities exist for startups to establish themselves in this burgeoning space.

- Issuance: Similar to the rise of corporate charge cards, we may witness a surge in demand for corporate-issued stablecoins. This provides greater control over accounting and expense management. While orchestration networks may offer white-label stablecoin solutions, this presents a distinct opportunity for specialized issuance platforms, akin to companies like Lithic.

- Specialized Issuance: Just as credit card companies offer tiered reward programs (e.g., Chase Sapphire Reserve), we may see the emergence of specialized stablecoins with unique reward structures. This could involve partnerships with airlines, retailers, or other entities, creating new avenues for innovation and differentiation.

These trends are interconnected. As issuance diversifies, the demand for sophisticated orchestration services will increase. Conversely, the maturation of orchestration networks will lower the barriers to entry for new issuers. This symbiotic relationship will fuel the growth of the entire stablecoin ecosystem, creating substantial opportunities for startups and driving significant economic value.